Operate Diminishing Musharaka with cryptographic ownership tracking.

Diminishing Musharaka requires precise tracking of declining bank ownership and customer ownership across the financing term. ZeroH ships a productised template: contract-to-code decomposition, periodic share purchase enforcement, lease payment tracking, and verifiable ownership-transfer evidence. Sharia-aligned, regulator-evidencable.

Diminishing Musharaka is operationally complex

The contract is one structure on paper. In operations, it is three concurrent flows. Musharaka ownership, Ijarah lease, and periodic Bai (sale) of bank shares to customer. Without integrated tracking, errors compound across the financing term.

3

concurrent contractual flows per Diminishing Musharaka

Three flows, one contract, easy to drift

Musharaka share + Ijarah lease + periodic Bai share-purchase each require precise tracking. Most platforms handle one of these well; few handle all three with the cross-flow consistency that Sharia compliance demands.

120-360

discrete ownership-transfer events per 10-30 yr term

Periodic ownership transfer needs proof

Each share purchase transaction (customer buying a portion of bank ownership) must be properly documented, properly priced (against fair market value at the time), and properly evidenced for the Sharia board. Manual processes accumulate errors.

25 yrs

typical Diminishing Musharaka home financing term

Long-term contracts span regulatory change

A 25-year Diminishing Musharaka outlives multiple regulatory regimes. AAOIFI standards evolve. Local jurisdiction rules change. Without versioned, anchored evidence, you cannot reconstruct what compliance posture the contract operated under at any given moment.

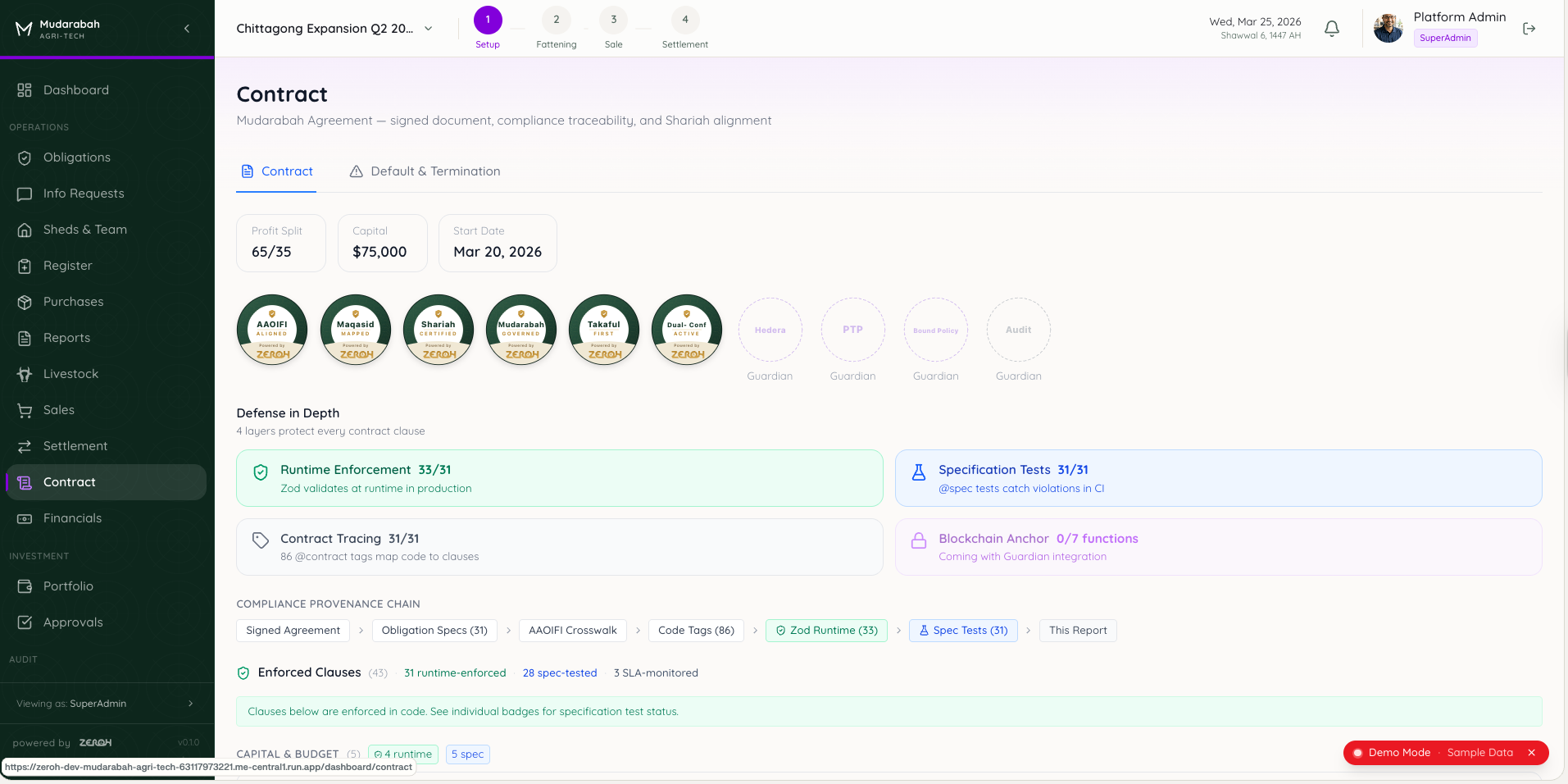

The ZeroH Diminishing Musharaka stack

Productised solution template with contract-to-code decomposition, three-flow workflow orchestration, and verifiable evidence at every ownership transfer.

ZeroH Platform. Diminishing Musharaka Template

LiveThree-flow workflow orchestration with on-chain ownership tracking

ZeroH decomposes Diminishing Musharaka into discrete obligations across the three flows. Musharaka, Ijarah, periodic Bai. Each ownership transfer is captured, priced, evidenced, and anchored. Sharia board oversight surface dedicated. Full lifecycle from origination through final ownership transfer.

- ✓Diminishing Musharaka contract decomposition across three flows

- ✓Periodic ownership transfer workflows with fair-market-value pricing

- ✓Ijarah lease payment tracking integrated with share-purchase events

- ✓Sharia board oversight surface for ongoing supervision

- ✓Tamper-evident evidence at every ownership transfer

- ✓Aligned to AAOIFI Sharia Standards 12 (Musharakah) and 9 (Ijarah)

ZeroH Disclosure

AlphaCustomer privacy preserved through the contract lifecycle

Diminishing Musharaka touches sensitive customer data. Income, valuation, family circumstances. ZeroH Disclosure ensures cross-border processing respects data residency, with cryptographic proof of redaction for every external interaction (third-party valuers, auditors, regulators).

- ✓Customer PII redaction across the financing term

- ✓Selective disclosure with cryptographic proof (in development) for auditor and Sharia board sharing

- ✓Cross-border data residency for cross-jurisdictional structures

- ✓DPIA-grade evidence for GDPR / Gulf data protection regimes

Ask Ali

BetaSharia escalations during the long-term contract

Diminishing Musharaka structures last decades. AAOIFI standards evolve. Local jurisdiction rules change. Ask Ali handles the Sharia-question moments. Multi-madhahib reasoning on regulatory updates, source-attributed analysis, edge-case escalation to Sharia board.

- ✓AAOIFI Musharakah and Ijarah clause-level analysis

- ✓Multi-madhahib reasoning on long-term contract edge cases

- ✓Regulatory change impact analysis for active contracts

- ✓Source-attributed answers for Sharia board escalation

Three flows, one verifiable lifecycle

ZeroH operates Diminishing Musharaka as it is contracted. Three concurrent flows, cross-consistent, on-chain.

The structure your Sharia board approved is the runtime

The Diminishing Musharaka contract is decomposed into machine-enforceable obligations across all three flows. The Sharia-approved structure becomes the operational runtime. No drift between contract and execution.

Each share purchase: priced, evidenced, anchored

When the customer purchases a periodic share of bank ownership, ZeroH captures fair market value, executes the share-purchase obligation, generates evidence, and records it tamper-evidently. The ownership ledger updates atomically.

Every contract state, at every moment, verifiable years later

For a 25-year contract, ZeroH gives auditors and regulators the ability to reconstruct exact contract state at any prior moment. What standards were in force, what rate applied, what evidence was filed, what Sharia view governed. Cryptographic provenance survives regulatory regime change.

Frequently Asked Questions

Explore by Role

See how ZeroH serves different roles in your organisation.

CISOs

ZeroH gives CISOs at regulated banks, insurers, and asset managers a verifiable safety layer for the AI tools their staf

Data Protection Officers

ZeroH gives DPOs cryptographic, third-party-verifiable evidence designed to show that personal data was redacted before

AI Risk Officers

ZeroH gives AI Risk Officers cryptographic, third-party-verifiable evidence of AI governance. Aligned to PRA SS1/23 mode

Compliance Officers

ZeroH automates compliance tracking, surfaces regulatory changes before they become gaps, and generates audit-ready evid

Shariah Boards

ZeroH maintains a living record of every fatwa, approval condition, and parameter boundary. Your board focuses on schola

CFOs and Finance Leaders

Self-service deployment in weeks, not months. No consultants required. Verifiable evidence that satisfies regulators and

Risk Managers

ZeroH maps Shariah non-compliance risk alongside your operational, regulatory, and reputational risk frameworks. One pla

Auditors

Continuous Shariah compliance monitoring that flags product drift the moment it occurs, generates audit-ready evidence t

Digital Bank Formation

ZeroH is validated inside the Qatar Financial Centre Digital Assets Lab for verifiable Shariah-compliance audit trails i

Explore by Region

See how ZeroH operates in key Islamic finance markets.

Saudi Arabia

SAMA's Shariah Governance Framework requires independent Shariah boards, documented compliance processes, and structured

United Arab Emirates

CBUAE, ADGM, and DIFC each operate distinct regulatory frameworks for Islamic finance and digital assets. ZeroH maintain

Qatar

ZeroH is validated inside the Qatar Financial Centre Digital Assets Lab — Qatar's international financial hub. QCB's AI

Bahrain

The Central Bank of Bahrain's Rulebook Volume 2 sets some of the most detailed Shariah governance requirements globally.

Kuwait

Kuwait's Islamic banking sector manages over $140B in assets under CBK Shariah governance instructions and AAOIFI standa

Malaysia

BNM's Shariah Governance Policy Document, the Securities Commission's Capital Markets Plan 2026-2030, and PDPA create ov

Indonesia

OJK Shariah governance regulations, DSN-MUI fatwa requirements, and Bank Indonesia oversight create layered compliance o

Bangladesh

With $47B in Islamic banking assets, 10 full-fledged Islamic banks, and over 50 Islamic banking windows, Bangladesh carr

Pakistan

With $50B+ in Islamic banking assets, five full-fledged Islamic banks, and an SBP-mandated Shariah governance framework,

United Kingdom

With $100B+ in Islamic finance assets, five dedicated Islamic banks, and an FCA regulatory framework that demands docume

Verifiable Diminishing Musharaka. Built once, evidenced forever.

Schedule a demo to see how the ZeroH Diminishing Musharaka template operates the contract as it is structured. Three flows, cross-consistent, on-chain from day one.